Most people need to save more — often a lot more — to build a nest egg that can meet their needs. Many financial experts recommend putting away 10 to 15 percent of your pay for retirement. There’s a relatively painless way to reach that goal.

Take small steps

• Begin by contributing enough to receive your employer’s matching contribution

• Consider gradually raising your contribution amount to 10 percent or higher

• Raise your plan contributions once a year by an amount that’s easy to handle, on a date that’s easy to remember—say, 2 percent on your birthday. Thanks to the power of compounding (the earnings on your earnings), even small, regular increases in your plan contributions can make a big difference over time.

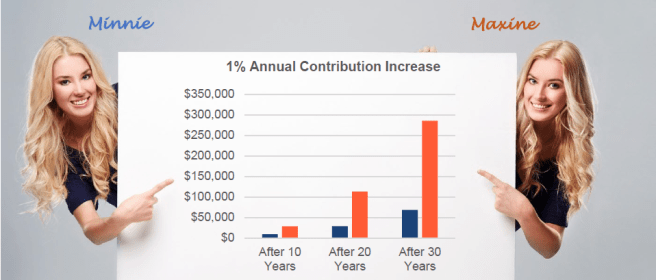

A little more can mean a lot

Let’s look at Minnie and Maxine. These hypothetical twin sisters do almost everything together. Both work for the same company, earn the same salary ($30,000 a year), and start participating in the same retirement plan at age 35. In fact, just about the only difference is their savings approach:

Minnie contributes 2 percent of her pay each year. Her salary rises 3 percent a year (and her contributions along with it), and her investments earn 6 percent a year on average. So, after 30 years of diligent saving, Minnie will reach retirement with a nest egg worth $68,461.

Maxine gets the same pay raises, saves just as diligently, and has the same investments as her sister—except for one thing: She starts contributing 2 percent, but raises her rate by 1 percent each year on her birthday until she reaches 10 percent. She will keep saving that 10 percent for the next 22 years, until she retires by Minnie’s side.

Maxine tells Minnie that she’s never really noticed a difference in take-home pay as her savings rate rises. Instead, she looks forward to having $285,725 in her retirement fund by age 65.

Think ahead and act now. To increase your deferral percentage, contact your HR department today.

This memo was contributed by Transamerica.

This example is hypothetical and does not represent the performance of any fund. Regular investing does not guarantee a profit or protect against a loss in a declining market. Past performance does not guarantee future results. Initial tax savings on contributions and earnings are deferred until distribution. You should evaluate your ability to continue saving in the event of a prolonged market decline, unexpected expenses, or an unforeseeable emergency. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation.

ACR# 3330000 11/20